Factors to Consider When Planning for Retirement

One crucial factor to consider when planning for retirement is determining your desired lifestyle during your golden years. It’s essential to evaluate what kind of activities you envision yourself doing, where you want to live, and how much you expect to spend on leisure and travel. Understanding your lifestyle goals will help you calculate the approximate amount of savings needed to support that lifestyle throughout your retirement years.

Another important consideration is assessing your current financial situation and determining how much you need to save each month to reach your retirement goals. Take into account your current income, expenses, assets, and liabilities to create a realistic budget that aligns with your retirement objectives. Setting specific savings targets and regularly monitoring your progress can help you stay on track to achieve a comfortable retirement.

Income Sources in Retirement

When planning for retirement, it is crucial to consider various income sources that can sustain you during your post-employment years. One common income source for retirees is Social Security benefits, which are typically based on your earnings history and the age at which you choose to start receiving them. It is important to understand how Social Security benefits work and how they will factor into your overall retirement income.

Another income source to consider is pensions from your employer or a former employer. Pensions provide a steady stream of income during retirement, usually based on your years of service and salary history with the company. Understanding the details of your pension plan and how it will contribute to your overall income in retirement is essential for effective financial planning.

Retirement Calculator When planning for retirement, it is crucial to consider various income sources that can sustain you during your post-employment years. Social Security benefits and pensions from your employer are common income sources to understand for effective financial planning.

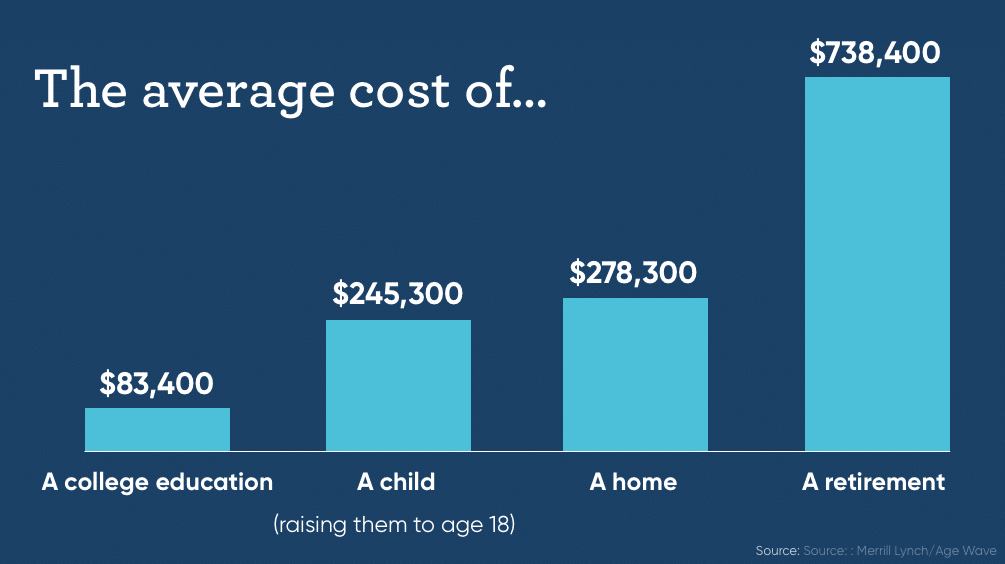

Cost of Living in Retirement

When planning for retirement, it is crucial to carefully consider the cost of living during your post-employment years. Many individuals underestimate the expenses that come with maintaining a comfortable lifestyle after retirement. It is essential to take into account factors such as housing costs, utilities, healthcare expenses, food, transportation, and leisure activities.

Ensuring that you have a solid understanding of your anticipated cost of living in retirement can help you better manage your finances and make informed decisions about your retirement savings and investment strategies. By accurately estimating your future expenses and creating a realistic budget, you can ensure that your retirement savings will be sufficient to cover your needs and maintain your desired standard of living.

Healthcare Expenses in Retirement

As individuals plan for retirement, one significant aspect that requires careful consideration is the potential healthcare expenses they may face during their post-employment years. Healthcare costs tend to increase with age, and retirees often find themselves needing more medical care as they grow older. It is crucial for individuals to account for these expenses when creating a retirement budget to ensure that they are adequately prepared for any healthcare needs that may arise.

From routine check-ups to unexpected medical emergencies, healthcare expenses can quickly add up and impact a retiree’s financial stability. Factors such as health conditions, prescription medications, and long-term care can significantly contribute to overall healthcare costs in retirement. Understanding these potential expenses and planning accordingly can help retirees navigate their healthcare needs with confidence and peace of mind.

Debt Management in Retirement

Managing debt in retirement is a critical aspect that individuals need to carefully navigate. It is essential to assess existing debts and create a repayment strategy that aligns with the fixed income typically available during retirement. Prioritizing high-interest debts can help in reducing overall interest payments and free up more funds for other expenses. Additionally, considering debt consolidation or refinancing options could be beneficial in streamlining payments and potentially lowering interest rates.

As individuals transition into retirement, it is crucial to be vigilant about taking on new debt. While some level of debt may be inevitable, especially for significant expenses like healthcare or home repairs, it is essential to evaluate the necessity and affordability of new debt. Setting a budget and regularly reviewing expenses can help in identifying areas where debt can be minimized or avoided altogether. By maintaining a proactive approach to debt management, retirees can work towards a more secure financial future.

SIP Calculator Managing debt in retirement is crucial. Assess existing debts, prioritize high-interest ones, and consider consolidation or refinancing. Be cautious about taking on new debt, set a budget, and review expenses regularly to minimize or avoid debt. A proactive approach to debt management leads to a more secure financial future.

Longevity Risk in Retirement

We often underestimate the impact that longevity risk can have on our retirement plans. Longevity risk refers to the chance that we may outlive our retirement savings, leaving us financially vulnerable in our later years. With life expectancies increasing and healthcare advancements allowing people to live longer, it’s essential to consider how to mitigate this risk.

To address longevity risk in retirement, individuals may need to reevaluate their retirement savings goals and strategies. This could involve adjusting investment portfolios to ensure they are balanced between growth and stability, as well as considering options like annuities that provide a guaranteed income stream for life. It’s crucial to factor in the possibility of a longer retirement period when crafting a financial plan to ensure financial security throughout one’s lifetime.

Investment Strategies for Retirement

When it comes to planning for retirement, one of the critical aspects to consider is the investment strategies that will help you secure your financial future. Diversification is key in minimizing risk and maximizing returns. Allocating your assets across different types of investments can help you weather market fluctuations and achieve your long-term financial goals.

Another important factor to keep in mind is to regularly review and adjust your investment portfolio as needed. As you move closer to retirement, it may be prudent to shift your investments towards more conservative options to protect your savings. Working with a financial advisor can provide valuable guidance on creating an investment strategy tailored to your specific needs and goals.

Social Security Benefits in Retirement

Social Security benefits play a crucial role in providing financial stability during retirement years. Understanding how these benefits work and when to begin claiming them can significantly impact one’s overall retirement income. It’s important to consider factors such as the full retirement age, early retirement options, and the potential impact of delaying benefits.

Additionally, knowing how Social Security benefits are calculated based on work history and earnings can help retirees make informed decisions about their claiming strategy. While these benefits may not cover all expenses in retirement, they can serve as a reliable source of income to supplement other retirement savings and investments.

Open Demat Account Social Security benefits are crucial for financial stability in retirement. Understanding when to claim benefits based on factors like full retirement age and work history can impact overall income. While not covering all expenses, these benefits can supplement retirement savings and investments.

Retirement Savings Vehicles

When planning for retirement, it is crucial to consider the various savings vehicles available to help you reach your financial goals. One common option is an Individual Retirement Account (IRA), which allows individuals to save for retirement with tax advantages. There are two main types of IRAs: traditional IRAs, where contributions may be tax-deductible, and Roth IRAs, where withdrawals in retirement are tax-free.

Another popular retirement savings vehicle is an employer-sponsored 401(k) plan. This type of plan allows employees to contribute a portion of their pre-tax salary to a retirement account, often with employer matching contributions. 401(k) plans offer tax advantages and the potential for investment growth over time, making them a valuable tool in building a secure financial future for retirement.

Investment App When planning for retirement, it is crucial to consider the various savings vehicles available to help you reach your financial goals. One common option is an Individual Retirement Account (IRA), which allows individuals to save for retirement with tax advantages. There are two main types of IRAs: traditional IRAs, where contributions may be tax-deductible, and Roth IRAs, where withdrawals in retirement are tax-free.

Another popular retirement savings vehicle is an employer-sponsored 401(k) plan. This type of plan allows employees to contribute a portion of their pre-tax salary to a retirement account, often with employer matching contributions. 401(k) plans offer tax advantages and the potential for investment growth over time, making them a valuable tool in building a secure financial future for retirement.

Estate Planning for Retirement

Many individuals overlook estate planning when preparing for retirement. However, it is a crucial aspect of ensuring that your assets are distributed according to your wishes after you pass away. Estate planning involves creating legal documents such as wills, trusts, and powers of attorney to protect your assets and provide for your loved ones.

One important consideration in estate planning is minimizing the tax burden on your estate. By structuring your assets and investments in a tax-efficient manner, you can potentially reduce the amount of estate taxes that your heirs will have to pay. Consulting with a financial advisor or estate planning attorney can help you navigate the complex laws and regulations surrounding estate taxes and ensure that your assets are distributed according to your wishes.